Automate Your Trading Strategy: A Step-by-Step Guide

The world of trading, once dominated by floor-based brokers and manual order execution, has been dramatically reshaped by technology. Today, a significant portion of trading activity is executed through automated systems. Automating your trading strategy can offer a multitude of benefits, from increased speed and efficiency to the elimination of emotional biases that often plague human traders. But what exactly does it mean to automate a trading strategy, and how can you go about it? This comprehensive guide will delve into the intricacies of algorithmic trading, providing you with the knowledge and steps needed to transform your trading ideas into a functioning automated system.

According to Statista, the global algorithmic trading market was valued at approximately $18.1 billion in 2022 and is projected to grow significantly in the coming years. This surge highlights the increasing adoption and importance of automated trading in modern financial markets.

What is Algorithmic Trading?

At its core, algorithmic trading, often shortened to algo-trading, is a method of executing orders using automated, pre-programmed trading instructions that account for variables such as time, price, and volume. These algorithms are designed to automatically place orders when certain conditions are met, aiming to achieve optimal execution prices or to trade large volumes at once with minimal market impact.

These systems can be incredibly sophisticated, capable of analyzing vast amounts of market data in real-time, identifying trading opportunities, and executing trades faster than any human could. They are not sentient beings; rather, they are complex sets of rules and mathematical models designed to exploit market inefficiencies or execute predefined trading plans.

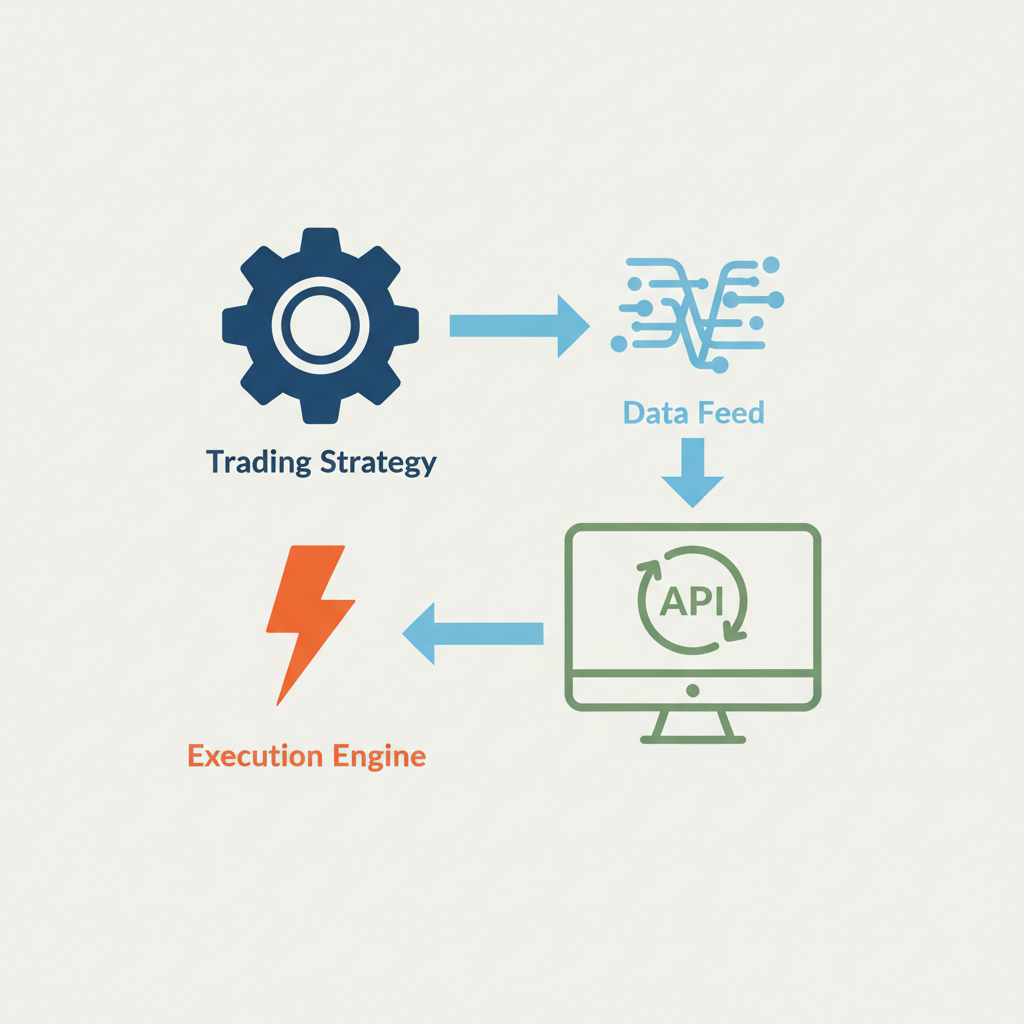

The Components of an Algorithmic Trading System

Before diving into the automation process, it's essential to understand the key components that make up an algorithmic trading system:

- Trading Strategy: The set of rules and logic that dictates when to buy, when to sell, how much to trade, and how to manage risk. Your strategy could be based on technical indicators, fundamental analysis, statistical arbitrage, or a combination of factors.

- Data Feed: Algorithmic trading relies on real-time market data, including prices, volumes, order book information, and news. A reliable and fast data feed is crucial for making timely trading decisions.

- Trading Platform/Brokerage: You need a platform that allows you to connect your algorithm to the market. This typically involves using a brokerage that offers an Application Programming Interface (API) to facilitate communication between your trading software and their execution servers.

- Execution Engine:The software that takes the signals generated by your strategy and translates them into actual buy or sell orders, sending them to the broker's execution system.

- Backtesting Engine:Crucial for validating your strategy's potential profitability and robustness. A backtesting engine simulates your strategy on historical data to see how it would have performed.

- Risk Management Module: An integral part of any trading system, this module defines rules for position sizing, stop-loss orders, take-profit levels, and overall portfolio risk.

Why Automate Your Trading Strategy?

The decision to automate a trading strategy is driven by several compelling advantages:

1. Speed and Efficiency

Automated systems can process information and execute trades at speeds that are impossible for humans. In fast-moving markets, a few seconds can mean the difference between a profitable trade and a losing one. Algorithms can monitor multiple markets and instruments simultaneously, react to price changes instantly, and execute orders with minimal latency.

2. Elimination of Emotional Biases

Fear, greed, impatience, and overconfidence are common emotional pitfalls that can lead to poor trading decisions. An automated system, driven by logic and predefined rules, is immune to these emotions. It will execute trades strictly according to its programming, regardless of market sentiment or personal feelings. This consistency is a significant advantage in maintaining a disciplined trading approach.

3. Backtesting and Optimization

Before risking real capital, you can rigorously test your trading strategy using historical data. This backtesting process allows you to evaluate the potential profitability, drawdowns, and other performance metrics of your strategy under various market conditions. You can then optimize parameters to improve its performance.

4. Consistency and Discipline

Once a strategy is programmed, it will execute trades with unwavering consistency. This removes the temptation to deviate from the plan due to sudden market movements or gut feelings. Discipline is paramount in trading, and automation enforces it.

5. Scalability

Automated trading systems can be scaled to handle larger trade volumes or to monitor a wider array of markets and assets without a proportional increase in human effort. This allows traders to grow their operations more efficiently.

6. Reduced Transaction Costs

Some automated strategies, particularly those focused on high-frequency trading (HFT), can be designed to minimize transaction costs by executing trades at optimal times and prices, potentially taking advantage of small price discrepancies.

Steps to Automate Your Trading Strategy

Automating your trading strategy is a multi-step process that requires careful planning, development, and testing. Here's a breakdown of the key stages:

Step 1: Develop a Trading Strategy

This is the most crucial step. Your strategy must be well-defined, logical, and have a demonstrable edge.

- Identify Your Edge: What makes your strategy unique? Is it a pattern recognition technique, a statistical anomaly, or a response to specific news events?

- Define Entry and Exit Rules:Be precise. For example, "Buy when the 50-day moving average crosses above the 200-day moving average, and the RSI is below 30. Sell when the price reaches 2% profit or 1% loss."

- Determine Position Sizing: How much capital will you allocate to each trade? This is critical for risk management.

- Implement Risk Management: Define stop-loss levels, take-profit targets, and maximum drawdown limits.

- Choose Your Market and Timeframe: Will you trade stocks, forex, futures, or cryptocurrencies? What timeframes (e.g., 1-minute, hourly, daily) will you focus on?

Step 2: Choose Your Programming Language and Tools

Several programming languages are popular for algorithmic trading due to their libraries and ease of use for data analysis and mathematical operations.

- Python: Widely used for its extensive libraries like

pandasfor data manipulation,NumPyfor numerical operations,scikit-learnfor machine learning, andMatplotlibfor visualization. Frameworks likeBacktraderandZiplineare specifically designed for backtesting trading strategies. - C++: Preferred for high-frequency trading (HFT) due to its speed and efficiency, though it has a steeper learning curve.

- Java: Another robust option, often used in institutional trading environments.

- MQL4/MQL5: Specialized languages for the MetaTrader trading platform, popular among retail forex traders.

Skip MQL: Use Any Language with FxSocket

MQL4 and MQL5 are powerful but force you into MetaTrader's ecosystem. If you already know Python, JavaScript, Go, or Rust, you don't need to learn a new language. FxSocket exposes MT4 and MT5 through a standard REST API and WebSocket, so you can write your trading logic in whatever language you're most productive in, using the libraries and frameworks you already know.

Step 3: Acquire Market Data

Your algorithm needs access to reliable market data.

- Historical Data: Essential for backtesting. You can obtain this from your broker, dedicated data providers, or sometimes freely available sources (though free data may have quality limitations).

- Real-Time Data: For live trading, you need a continuous stream of up-to-date market prices and other relevant information. Brokers typically provide this through their APIs.

Historical and Real-Time Data from One API

With FxSocket, both historical and real-time data come from the same API. Pull years of OHLC candles (M1 through MN1) via the PriceHistory endpoint for backtesting, then switch to the WebSocket stream for live ticks and price feeds, all with a single API key. Data comes directly from your broker's MetaTrader server, so you're backtesting on the exact prices you'll trade on. Learn more about backtesting with FxSocket →

Step 4: Backtest Your Strategy

This is where you rigorously test your strategy's performance on historical data.

- Simulate Trades:Your backtesting engine will replay historical market data, executing your strategy's rules and recording the hypothetical trades.

- Analyze Performance Metrics: Evaluate key metrics such as total return, win rate, profit factor, maximum drawdown, and Sharpe ratio.

- Iterate and Optimize:Based on the results, refine your strategy's parameters or rules. Be cautious of overfitting, where a strategy performs exceptionally well on historical data but fails in live trading because it's too tailored to past specific conditions.

Step 5: Connect to a Broker's API

To execute trades automatically, your algorithm needs to communicate with a brokerage.

- Choose a Broker: Select a broker that offers an API and supports the markets and instruments you intend to trade. Popular brokers for algorithmic trading include Interactive Brokers, Alpaca, and OANDA (for forex).

- Understand the API:Familiarize yourself with the broker's API documentation. This will guide you on how to place orders, retrieve account information, and receive market data.

- Implement Order Execution: Write code to send buy/sell orders, specify order types (market, limit, stop), quantities, and other parameters to your broker via the API.

Connect to MT4/MT5 Without the Headache

If you trade on MetaTrader, the traditional path is writing Expert Advisors in MQL and running them on a VPS. FxSocket removes that entire layer. We host cloud-based MT4/MT5 terminals and expose them through a REST API and WebSocket. Your algorithm sends standard HTTP requests to place orders, manage positions, and stream prices, from Python, Node.js, Go, or any language. No MQL, no VPS, no terminal running on your desktop.

import requests

API_KEY = "fxs_live_..."

ACCOUNT_ID = "your_account_id"

BASE = "https://api.fxsocket.com/mt5"

# Place a market buy order on EURUSD

response = requests.post(

f"{BASE}/{ACCOUNT_ID}/OrderSend",

headers={"X-API-Key": API_KEY},

json={

"symbol": "EURUSD",

"operation": "Buy",

"volume": 0.1,

"stopLoss": 1.0720,

"takeProfit": 1.0950,

},

)

print(response.json())Step 6: Paper Trading (Forward Testing)

Before deploying your algorithm with real money, it's crucial to test it in a simulated live environment.

- Simulated Account:Most brokers offer "paper trading" or "demo" accounts that use live market data but with virtual funds.

- Monitor Performance: Run your algorithm on this simulated account for a sufficient period (weeks or months) to observe its real-time performance, identify any bugs, and gain confidence in its operation.

FxSocket works identically with both demo and live MetaTrader accounts. Connect a demo account, test your strategy against live market data, and when you're ready, switch to a live account by changing one parameter. Your code stays the same.

Step 7: Live Trading and Monitoring

Once you are confident in your strategy's performance during paper trading, you can transition to live trading.

- Start Small: Begin with a small amount of capital that you can afford to lose. This allows you to experience the psychological aspects of live trading with an automated system.

- Continuous Monitoring: Even though the system is automated, regular monitoring is essential. Keep an eye on connectivity, performance, errors, and market changes.

- Regular Review and Updates:Periodically review your strategy's performance and market conditions. You may need to adjust parameters or even redesign the strategy if its edge diminishes.

Popular Algorithmic Trading Strategies

While the possibilities are vast, several common types of algorithmic trading strategies exist:

1. Trend Following

These strategies aim to profit from established market trends. Algorithms identify an uptrend and buy, or a downtrend and sell (short), holding the position until the trend shows signs of reversing. Indicators like moving averages, MACD, and ADX are often used.

2. Mean Reversion

This strategy is based on the principle that prices tend to revert to their historical average over time. Algorithms identify assets that have moved significantly away from their mean and bet on them returning to that average. Statistical indicators like Bollinger Bands and Z-scores are commonly employed.

3. Arbitrage Strategies

Arbitrage involves exploiting tiny price differences for the same asset in different markets or forms. These opportunities are often short-lived and require high-speed execution, making them suitable for HFT.

4. Market Making

Market makers provide liquidity to the market by simultaneously placing buy (bid) and sell (ask) orders for an asset. They profit from the spread (the difference between the bid and ask prices). This requires sophisticated algorithms to manage inventory and risk.

5. Event-Driven Strategies

These algorithms are designed to capitalize on predictable price movements that may occur in response to specific events, such as earnings announcements, mergers, or economic data releases.

6. Sentiment Analysis

With the rise of natural language processing (NLP), algorithms can now analyze news articles, social media feeds, and other text-based data to gauge market sentiment. If sentiment turns positive, the algorithm might buy; if negative, it might sell.

Challenges and Considerations

While automation offers significant advantages, it's not without its challenges:

1. Technical Complexity

Developing, implementing, and maintaining an algorithmic trading system requires strong programming skills, a deep understanding of financial markets, and robust IT infrastructure.

2. Data Quality and Latency

The performance of your algorithm is heavily dependent on the quality and speed of your market data. Inaccurate or delayed data can lead to flawed trading decisions.

3. Overfitting

A strategy that performs perfectly on historical data but fails in live trading is a common problem. It indicates that the strategy has been too finely tuned to past market noise rather than genuine predictive patterns.

4. Market Regimes and Strategy Decay

Markets are dynamic. A strategy that works well in one market condition (e.g., a trending market) may perform poorly in another (e.g., a sideways market). The effectiveness of a strategy can also decay over time as other market participants identify and exploit the same inefficiencies.

5. Execution Risk

Even with automation, there's still a risk that trades may not be executed as intended due to factors like slippage, system downtime, or broker issues.

Minimize Infrastructure and Execution Risk

Many of these challenges (server management, connectivity issues, MetaTrader terminal crashes) disappear when you use a managed API like FxSocket. Your terminals run in the cloud with 99.99% uptime and sub-30ms execution. No VPS to manage, no Windows server to patch, no terminal to restart at 3am. You focus on the strategy; FxSocket handles the infrastructure.

6. Regulatory Landscape

Algorithmic trading is subject to various regulations depending on the jurisdiction and the type of trading. It's important to stay informed about relevant rules and compliance requirements.

7. Cost of Infrastructure

Setting up a robust algorithmic trading system can involve costs for data feeds, trading platforms, servers, and potentially specialized software. A managed API approach consolidates these costs: FxSocket starts at €12/account/month for the complete stack: cloud terminals, REST API, WebSocket streams, and historical data access.

Ethical Considerations in Algorithmic Trading

- Market Stability: High-frequency trading (HFT) strategies, while legal, have been criticized for potentially exacerbating market volatility during periods of stress. The Flash Crash of 2010, where the Dow Jones Industrial Average plummeted and recovered rapidly within minutes, highlighted the potential impact of high-speed automated trading.

- Fairness: Ensuring that all market participants have access to fair trading opportunities is crucial. Concerns have been raised about whether certain HFT strategies might gain an unfair advantage through privileged access to data or faster connections.

- Transparency: While proprietary algorithms are naturally confidential, regulators and market participants often seek a degree of transparency to understand market dynamics and prevent manipulative practices.

Conclusion

Automating your trading strategy is a powerful way to enhance efficiency, discipline, and potentially profitability in the financial markets. It involves a systematic approach, starting with a well-defined strategy, moving through development and rigorous testing, and culminating in live deployment and continuous monitoring.

The journey from a trading idea to a fully automated system requires dedication, continuous learning, and a commitment to risk management. By understanding the components, steps, and challenges involved, traders can leverage the power of technology to navigate the complexities of the modern financial landscape and pursue their trading objectives with a more robust and systematic approach.

Ready to Automate Your MetaTrader Strategy?

FxSocket gives you a REST API and WebSocket for MT4 and MT5, so you can build, backtest, and deploy automated strategies in Python, Node.js, Go, or any language. No MQL. No VPS. Start making your first API call in under 5 minutes.

Frequently Asked Questions

What is the difference between algorithmic trading and high-frequency trading?

Algorithmic trading is a broad term for using computer programs to execute trades based on predefined instructions. High-frequency trading (HFT) is a subset of algorithmic trading that focuses on executing a large number of orders at extremely high speeds, often holding positions for fractions of a second. HFT strategies typically rely on powerful hardware, low-latency connections, and sophisticated algorithms to exploit tiny price discrepancies.

Do I need to be a programmer to automate my trading strategy?

While advanced programming skills are beneficial, especially for complex strategies, it's not strictly mandatory. There are platforms and tools that offer more user-friendly interfaces, allowing traders to build strategies using visual scripting or by configuring pre-built modules without extensive coding. However, for custom or sophisticated strategies, coding in languages like Python is often necessary.

How much money do I need to start automated trading?

The amount of capital required varies significantly depending on the trading strategy, the markets you trade, and the broker you use. Some brokers allow you to start with very small amounts, while others have higher minimum deposit requirements. It's crucial to start with an amount you are comfortable losing, especially during the initial learning and testing phases. Many traders begin with paper trading accounts before committing real capital.

What are the biggest risks in automated trading?

The biggest risks include:

- Technical failures: System crashes, connectivity issues, or bugs in the code can lead to unintended trades or missed opportunities.

- Overfitting: A strategy that works well on historical data but fails in live markets.

- Slippage: The difference between the expected execution price and the actual price.

- Data errors: Inaccurate or delayed market data can lead to flawed trading decisions.

- Strategy decay: The strategy may become less effective over time as market conditions change.

Can automated trading guarantee profits?

No, automated trading cannot guarantee profits. Like any form of trading, it involves risk. An automated system executes a strategy, and the profitability of that strategy depends on its design, the market conditions, and proper risk management. Automation helps execute a potentially profitable strategy with discipline and efficiency, but it does not inherently create profitability.